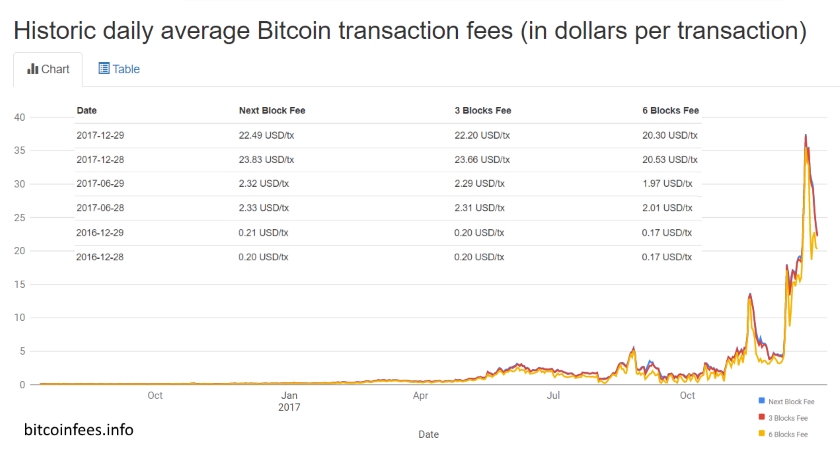

Bitcoin transaction fees have gone from around $2 a transaction in October to $37 in late December.

Bitcoin use in the real world may have started with the purchase of a pair of pizzas, but you’d be unlikely to see it used for such a minor exchange today.

That’s because as bitcoin has soared in popularity it’s become too expensive to use in small transactions.

The problem came to a head in early December, when Steam, the popular downloadable video game store, announced it would stop accepting bitcoin payments for games, citing the currency’s volatility and high transaction fees. Steam relied on a bitcoin payment system called BitPay. Among BitPay’s other customers are Microsoft, online retailer NewEgg, and APMEX, which sells precious metals online.

Don’t blame BitPay for high bitcoin transaction costs

You might think that services like BitPay are to blame for bitcoin’s high transaction costs. After all, BitPay’s service, which lets merchants accept bitcoin as payment, is similar to a credit card processing service, and retailers are often complaining that credit card fees cut into their profits.

But the fees charged by BitPay and similar companies represent only a small portion of the total cost of a typical bitcoin transaction. For its part, BitPay charges merchants a 1% processing fee per transaction.

Instead, blame the bitcoin miners

So if it’s not BitPay and other bitcoin payment processors that are making transactions using the cryptocurrency so expensive, what is? Walpole points the finger at bitcoin miners.

Miners are the people or companies that record data in the bitcoin blockchain, the digital ledger that keeps track of all bitcoin transactions. Miners save those transactions in so-called blocks; they complete a block by solving ever-more-complex cryptographic puzzles.

Mining has become an expensive proposition. It requires high-powered computers that use lots of energy. Miners are typically in the business to make money. They’re compensated for their services in three ways.

When they solve a particular puzzle and complete a block, they are awarded with newly created bitcoin. But they also collect fees from both individual bitcoin holders and from bitcoin payment processors such as BitPay.

Its those fees that have made using bitcoin so pricey.

Mining fees are skyrocketing

The first type of fee miners collect are mining or transaction fees. These fees in particular are surging.

At the end of September, the average bitcoin mining fee was around $2 per transaction. By December 21, average fees reached a high of around $37.

The surge in fees was a matter of supply and demand. As bitcoin’s price surged from $10,000 to $20,000, increasing numbers of people wanted to invest in the cryptocurrency. The upsurge in users and transactions increased the demand for miners’ services.

At the same time, supply is constrained. The blockchain system that underlies the cryptocurrency can only process around 3 to 7 transactions per second. So at any given moment, a greater number of transactions were competing for a relatively small number of slots in the ledger.

But another, related factor was at work too. Mining fees, which are paid by individual users to miners, are actually optional; bitcoin users don’t have to pay them. But they usually do, because the fees encourage miners to record their transactions sooner rather than later. The sooner you want a transaction written to the blockchain, generally the higher mining fee you’ll have to pay.

The advantage of having a transaction recorded quickly is that the sooner it’s recorded, the sooner you can spend or sell the coins you’ve received — and the sooner a merchant will mark a deal as completed. That speed can be important when using bitcoin to buy high-demand goods, like concert tickets, which can sell out fast.

But speeding the recording of bitcoin transactions has been particularly important in a volatile market such as the one the cryptocurrency has experienced in recent months. With the price of bitcoin fluctuating by hundreds or even thousands of dollars in mere hours or minutes, there’s a big benefit to being able to buy and sell coins sooner rather than later — and many bitcoin traders have been paying up for just that advantage.

There’s also network costs

In addition to mining fees, bitcoin users often have to pay a second fee that ultimately goes to miners, something called a network fee. Payment processors such as Bitpay and Coinbase collect such fees from consumers making purchases to pay miners to move funds from an individual customer’s bitcoin wallet address to that of a merchant. The payment processors add the fee to the transaction total.

Like mining fees, network costs fluctuate based on how busy the network is. Unlike mining fees, however, network charges aren’t optional; BitPay charges them on all transactions it handles to ensure that miners record those transactions as quickly as possible.

Source: businessinsider.com